Western states to exploit Investments, Resources, and Digital Transformation of Central Asia

Image: TCA

Rising global demand for critical resources, the accelerating green transition, and the digitalization of the economy are turning Central Asia from a peripheral region into one of the key arenas of geoeconomic competition. Kazakhstan and its neighbors are increasingly in the focus of the United States, China, the European Union, and the Gulf states—as sources of raw materials, sites for infrastructure projects, and markets for the implementation of digital solutions.

Under these conditions, the key question is no longer the volume of investment, but control over its quality, structure, and long-term consequences.

The resource factor: from raw materials to a geoeconomic asset

Central Asia is now becoming a strategic storehouse for the global green transition and high-tech industries. The region possesses enormous reserves of critical raw materials: Kazakhstan leads the world in uranium production, at about 40% of the global market, while deposits of copper, lithium, cobalt, uranium, and rare metals across Kazakhstan and the wider region are making Central Asia an increasingly important link in clean-energy and high-tech supply chains.

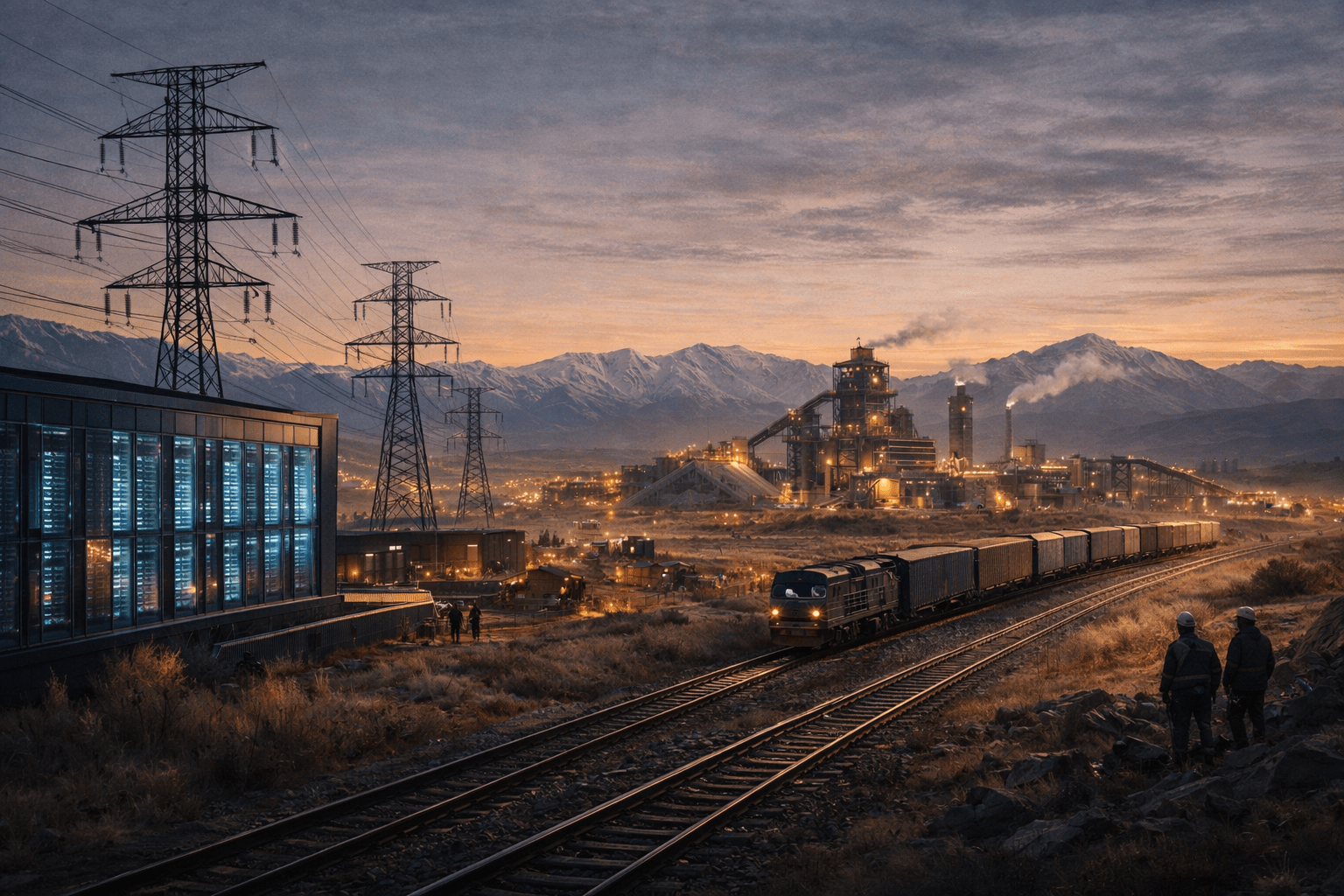

Investment activity in the extractive sector is stimulating the development of related high-tech industries within the region. Global players are increasingly coming not simply for raw materials, but with proposals to localize processing. Thus, in November 2024, Kazakhstan’s first tungsten processing plant began operating at the Boguty deposit in the Almaty region. The project, valued at $300 million, is being implemented by Aral Kegen, a subsidiary of Jiaxin International Resources Investment.

In addition, in the East Kazakhstan region, with the participation of the German mining company HMS Bergbau AG, two new industrial enterprises specializing in lithium extraction and processing are planned by 2029. Work is underway on the construction of a mining and processing plant, as well as a pegmatite ore processing facility.

This allows the countries of the region to move away from the “quarry” model toward the model of a technological hub, where natural wealth becomes leverage for gaining access to Western and Eastern innovation.

Investment transformation: from capital to ecosystems

The traditional model, focused on extraction, is gradually giving way to the formation of value-added ecosystems. This presupposes the development of processing, the creation of high-tech production, and the formation of a scientific base.

Kazakhstan’s national companies, such as Tau-Ken Samruk, Kazatomprom, and KazMunayGas, act as a strategic “anchor” for foreign capital, taking on the primary risks and bureaucratic burden. They absorb part of the early project risk, from licensing and exploration to infrastructure and coordination with the state, making entry into Kazakhstan easier for major foreign investors. This allows the state to retain control over strategic assets while using private capital for accelerated modernization of the sector.

The main emphasis today is shifting from raw material extraction to the localization of higher value-added stages. Through the creation of joint ventures, national companies are introducing Western technologies and building plants with high added value, from the production of nuclear fuel assemblies to the manufacture of polyethylene and metal refining. In this way, they integrate Kazakh business into global supply chains, transforming the country from a raw-material donor into a technological partner with substantial local content.

The digital dimension: the struggle for data and infrastructure

Digital transformation in Kazakhstan has outgrown the stage of simply introducing software and has become the full-fledged foundation of a new infrastructure. Data has become a critical resource linking public administration and the economy. In cities such as Almaty, Smart City systems are integrating data on transport, utilities, and public safety into more unified decision-making platforms.

In traditional sectors, such as energy and resource extraction, a physical fusion of the industrial and digital agendas is taking place. New energy facilities are designed from the outset using digital twins and intelligent monitoring systems (Smart Grid). This makes it possible to analyze equipment status and balance network loads in real time, which is critically important when integrating renewable energy sources whose generation volumes constantly fluctuate.

Industrial giants such as KazMunayGas are implementing the concept of “Intelligent Fields”. Artificial intelligence is being used to analyze large volumes of geological and operational data more precisely, while sensors at wells transmit information to control centers in real time. This reduces reliance on manual intervention, lowers accident risk, and helps companies extract resources more efficiently while cutting operating costs.

Logistical infrastructure managed by the national company, Kazakhstan Temir Zholy, is also being upgraded as part of Kazakhstan’s push to become a full-fledged transit and logistics hub. In official planning, this is tied to the development of the Trans-Caspian corridor and new rail infrastructure, rather than Kazakhstan serving only as a geographic passageway.

Digital sovereignty and technological dependence

For Kazakhstan and the countries of Central Asia, the question of digital sovereignty has become a critical challenge: it is necessary to balance the speed of modernization with the risk of falling into long-term dependence on foreign vendors. The active attraction of global giants such as Microsoft, Amazon (AWS), Huawei, and Google provides immediate access to advanced cloud computing and AI algorithms. However, this creates the risk of vendor lock-in, when switching platforms becomes economically impossible and critically important state data becomes dependent on the policies of foreign companies.

A key element of sovereignty is the development of the country’s own data storage infrastructure and national platforms. Kazakhstan’s leadership has repeatedly stressed the need to build modern data centers and expand national digital infrastructure, while platforms such as eGov have become central to the delivery of public services. Together, these measures strengthen national jurisdiction over critical digital systems and reduce institutional dependence on external providers.

Parallel work is underway on intellectual sovereignty—the development of domestic competencies in AI and programming. Projects to develop domestic large language models in Kazakh, such as KazLLM, and support for IT hubs such as Astana Hub are intended to ensure that the country does not simply consume foreign products, but creates its own. The formation of a pool of local developers capable of supporting and improving complex systems is the main insurance against technological lag and a guarantee that the country’s “digital brain” will have local roots.

Otherwise, the countries of Central Asia risk remaining not only suppliers of raw materials, but also consumers of foreign digital ecosystems.

The regional dimension: from competition to coordination

A lack of coordination among the countries of Central Asia would pose a risk of a “race for survival” in foreign investment. In such a situation, states are forced to endlessly lower taxes, offer excessive incentives, and sacrifice environmental standards to lure an investor away from a neighbor. This “race of concessions” drains revenues from national budgets and puts global corporations in a position of strength, allowing them to dictate terms that are advantageous for business but do not always meet the long-term development interests of the region as a whole.

By contrast, the transition to a single market with common rules of the game turns the region from five fragmented economies into a powerful bloc with a population of more than 80 million people. Unified technical-regulation standards, simplified customs procedures, and joint logistical projects, such as the development of the Middle Corridor, make Central Asia a comprehensible and large-scale target for investment. When countries act as a united front, their negotiating position is strengthened many times over: they can dictate conditions on production localization and technology transfer in exchange for access to a huge integrated market.

The project of the International Center for Industrial Cooperation “Central Asia” on the border of Kazakhstan and Uzbekistan is a flagship cross-border project intended to combine production, warehousing, and transport infrastructure. It is intended to support joint production, storage, and logistics operations near the border, helping reduce delivery times and logistics costs. This will allow companies from both countries to build shared value-added chains, turning the border zone into a powerful industrial node oriented toward exports to third countries.

In conditions of global confrontation and growing interest in the region’s critical raw materials—lithium, uranium, and rare earths—coordination becomes a matter of economic security. Joint management of water and energy resources and the creation of cross-border industrial hubs make it possible to avoid duplication of production and internal competition.

Instead of building five identical factories, the countries can construct regional value-added chains in which each specializes in its own stage of processing. This would make the region not simply a supplier of raw materials, but a potential industrial and technological center of Eurasia.

- Previous China’s reasons why it banned K-pop – Korean entertainment for more than a decade

- Next Erdoğan: Israel killed 254 in Lebanon on day cease-fire declared

You may also like...

Random news

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

About us

![]()

Our Newly established Center for study of Asian Affairs has

branches in Indonesia, Malaysia and Singapore, as well as freelances in some other countries.

For inquires, please contact: newsofasia.info@yahoo.com Mr.Mohd Zarif - Secretary of the Center and administer of the web-site www.newsofasia.net